Ifrs 9 Deutsch

The IFRS ® Foundation is a notforprofit international organisation responsible for developing a single set of highquality global accounting standards, known as IFRS Standards Our mission is to develop standards that bring transparency, accountability and efficiency to financial markets around the world Our work serves the public interest by fostering trust, growth and longterm.

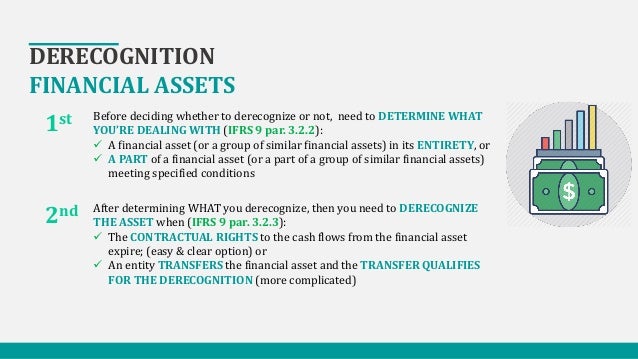

Ifrs 9 deutsch. IFRS 9544 An entity shall directly reduce the gross carrying amount of a financial asset when the entity has no reasonable expectations of recovering a financial asset in its entirety or a portion thereof A writeoff constitutes a derecognition event IFRS 9551 An entity shall recognise a loss allowance for expected credit losses on a. Where an institution’s opening balance sheet on the day that it first applies IFRS 9 reflects a decrease in Common Equity Tier 1 capital as a result of increased expected credit loss provisions, including the loss allowance for lifetime expected credit losses for financial assets that are creditimpaired, as defined in Appendix A to IFRS 9 as. Moved Permanently The document has moved here.

The IFRS ® Foundation is a notforprofit international organisation responsible for developing a single set of highquality global accounting standards, known as IFRS Standards Our mission is to develop standards that bring transparency, accountability and efficiency to financial markets around the world Our work serves the public interest by fostering trust, growth and longterm. IFRS 9 requires the institution to consider, where pertinent, the evolution of credit quality to maturity, which, from a risk management perspective, is a more transparent approach This approach should, in addition to satisfying the regulators, lead to better credit approval decisions, which also will improve over time as the supporting data. IFRS 9 states that firms shall apply a definition of default consistent with the definition used for internal credit risk management purposes However, there is a rebuttable presumption that a default does not occur later than when the instrument is 90 days pastdue The firm may rebut the presumption if it has reasonable and supportable.

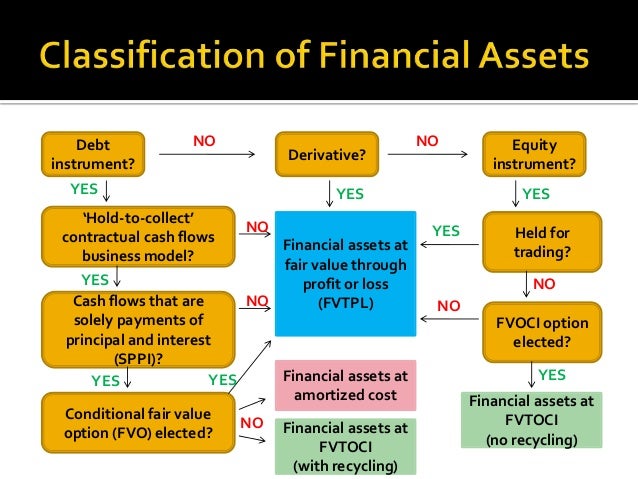

IFRS 9 A Quick Glance • IFRS 9 classifies financial assets into three categories • Measured at amortised cost • If the business model for holding the asset is to collect contractual cash flows and such cash flow are solely payments of principal and interest. IFRS 9, as amended, introduces a logical approach for the classification of financial assets, which is driven by cash flow characteristics and the business model in which an asset is held and a new, expectedloss impairment model that will require more timely recognition of expected credit losses. IFRS 9 and CECL Credit Risk Modelling and Validation A Prac £4761 starrating (13) International Financial Reporting Standards (IFRS) Deutsch £2495 starrating.

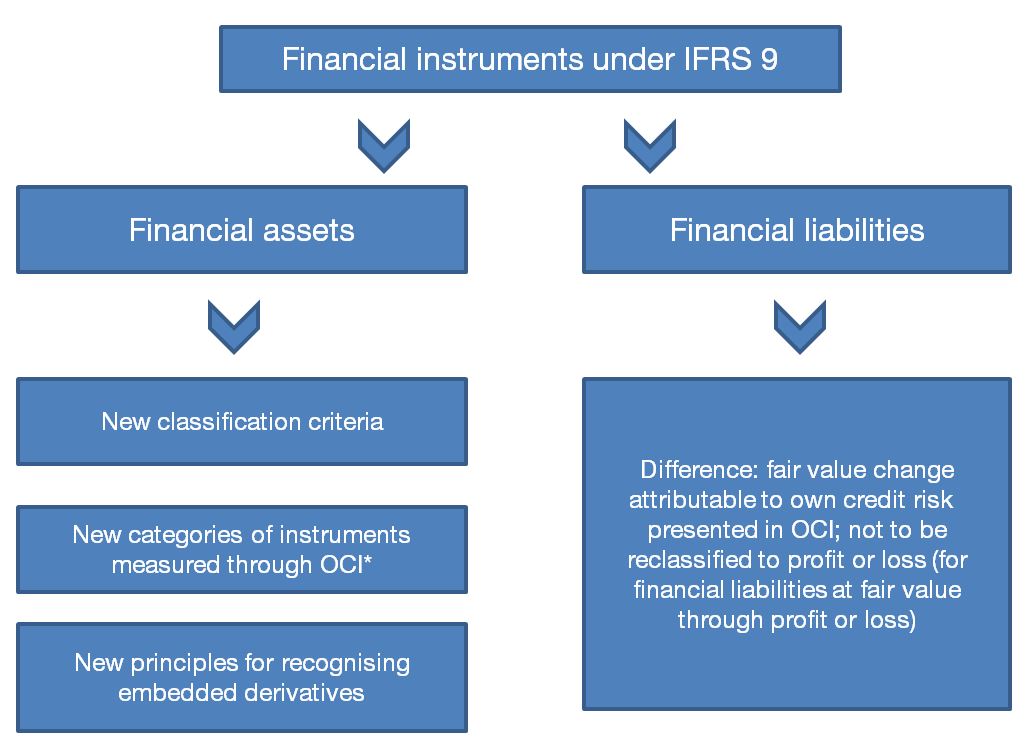

IFRS 9 and the complete ‘IFRS 9 for banks – Illustrative disclosures’ can be found at informpwccom We hope accountants, modellers and others involved in IFRS 9 implementation projects find this publication both practical and useful If you have any questions on the publication, or on other matters related to IFRS 9,. IFRS 9 replaces the rules based model in IAS 39 with an approach which bases classification and measurement on the business model of an entity, and on the cash flows associated with each financial asset This has resulted in i Elimination of the ‘held to maturity’, ‘loans and receivables’ and ‘availableforsale’ categories Instead, IFRS 9 introduces. Start studying IFRS 9 Financial Instruments Learn vocabulary, terms, and more with flashcards, games, and other study tools.

Compliance with the new regulations will already be mandatory for banks and corporates in January 18 Because of dependencies between IFRS 9 and the standard for booking insurance contracts IFRS 17 insurance companies are allowed to postpone the introduction of IFRS 9 until 21 at the latest Your Goals Resultsfocused interpretation. Contract often still can be measured at Amortized Cost Under IFRS 9, the entire contract will have to be measured at FVPL in all but a few cases The IFRS 9 model is simpler than IAS 39 but at a price— the added threat of volatility in profit and loss IFRS 9 replaces IAS 39’s patchwork of arbitrary bright line tests, accommodations,. IFRS 9 is an International Financial Reporting Standard (IFRS) published by the International Accounting Standards Board (IASB) It addresses the accounting for financial instrumentsIt contains three main topics classification and measurement of financial instruments, impairment of financial assets and hedge accountingThe standard came into force on 1 January 18, replacing the earlier.

19 edition (PDF 29 MB) 18 edition (PDF 27 MB) Supplements to annual Illustrative disclosures COVID19 supplement (PDF 25 MB) IFRS 12 supplement (PDF 12 KB) IFRS 15 supplement (PDF 15 MB) IFRS 16 supplement (PDF 18 MB) Annual Disclosure checklists edition (PDF 25 MB) 19 edition (PDF 26 MB) 18 edition (PDF 19 MB). Example 9 Reconciliation of changes in property, plant and equipment These examples are based on illustrative examples from the IFRS for SMEs They represent how reconciliation of gross carrying amount, accumulated depreciation and carrying amount of property, plant and equipment might be tagged using detailed XBRL tagging Inline XBRL;. This newsletter provides updates on IFRS developments that directly impact banks, and considers the potential accounting implications of regulatory requirements For our latest take on how banks are implementing the new financial instruments standard – IFRS 9 – read our online magazine, Realtime IFRS 9.

IFRS 9 accounting change confirmed As expected, the IASB confirmed the accounting for modifications of financial liabilities under IFRS 9 That is, when a financial liability measured at amortised cost is modified without this resulting in derecognition, a gain or loss should be recognised in profit or loss The gain or. Contract assets are subject to impairment requirements of IFRS 9 These requirements relate to measurement, presentation and disclosure with respect to impairment (IFRS ) Specifically, entities are required to recognise expected credit losses on their contract assets More about IFRS 15 See other pages relating to IFRS 15. BOZ IFRS 9 Guidance Note & Deferment of Compliance with Corporate Governance Directives Dear esteemed member, The Bank of Zambia has issued circulars on implementation of IFRS 9 for regulatory purposes and Deferment of Compliance with Corporate Governance Directives To access these two (2) documents, you can follow the links below and download.

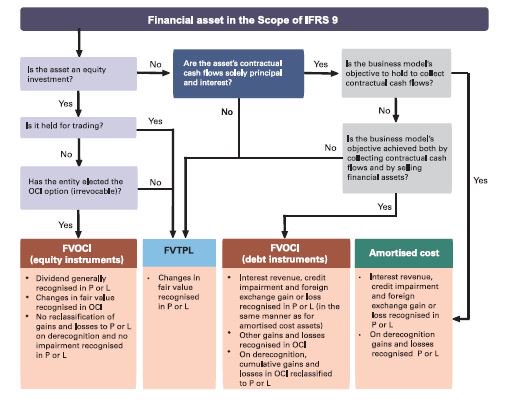

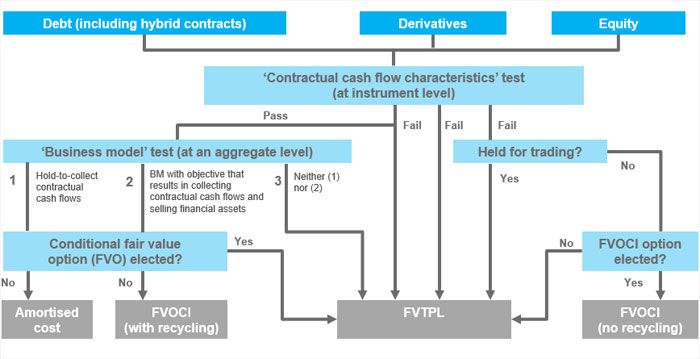

In order to determine the appropriate classification category under IFRS 9, entities must assess whether their financial assets meet the SPPI test at the date of initial recognition While financial assets that contained nonclosely related embedded derivatives under IAS 39 are more likely to fail this test, it is important that the contractual. IFRS 9 specifies how an entity should classify and measure financial assets, financial liabilities, and some contracts to buy or sell nonfinancial items IFRS 9 requires an entity to recognise a financial asset or a financial liability in its statement of financial position when it becomes party to the contractual provisions of the instrument. IFRS 9 requires the institution to consider, where pertinent, the evolution of credit quality to maturity, which, from a risk management perspective, is a more transparent approach This approach should, in addition to satisfying the regulators, lead to better credit approval decisions, which also will improve over time as the supporting data.

In order to determine the appropriate classification category under IFRS 9, entities must assess whether their financial assets meet the SPPI test at the date of initial recognition While financial assets that contained nonclosely related embedded derivatives under IAS 39 are more likely to fail this test, it is important that the contractual. Nized and measured in accordance with IFRS 9, Financial Instruments The benefit of the belowmarket rate of interest shall be measured as the difference between the initial carrying value of the loan determined in accordance with IFRS 9 and the proceeds received The benefit is accounted for in accordance with this Standard. Check out alternatives and read real reviews from real users.

IFRS 9 contains an option to designate, at initial recognition, a financial asset as measured at FVTPL if doing so eliminates or significantly reduces an ‘accounting mismatch’ that would otherwise arise from measuring assets or liabilities or recognising the gains and losses on them on different bases Financial assets designated at FVTPL. The issuance of IFRS 9, 15 and –to a certain extent –IFRS 16 was the result of getting many different views from those who were in favor and those who were against these standards We believe that because of these standards, the gap between IFRS and LUX GAAP is getting larger. IFRS 9 Financial Instruments issued on 24 July 14 is the IASB's replacement of IAS 39 Financial Instruments Recognition and Measurement The Standard includes requirements for recognition and measurement, impairment, derecognition and general hedge accounting.

And • assist companies in providing useful information to users of financial statements In Phase 2 of its project, the Board amended requirements in IFRS 9, IAS 39, IFRS 7, IFRS 4 Insurance Contracts and IFRS 16 Leases relating to. Compliance with the new regulations will already be mandatory for banks and corporates in January 18 Because of dependencies between IFRS 9 and the standard for booking insurance contracts IFRS 17 insurance companies are allowed to postpone the introduction of IFRS 9 until 21 at the latest Your Goals Resultsfocused interpretation. An entity applies IFRS 9 to such longterm interests before it applies paragraph 38 and paragraphs 4043 of this Standard In applying IFRS 9, the entity does not take account of any adjustments to the carrying amount of longterm interests that arise from applying this Standard.

Https//wwwcpdboxcom/If you want to learn more and get useful articles and news from me, sign up for my free newsletter at https//wwwcpdboxcom/ It is FREE. And (b) paragraph B63 of IFRS 15 on consideration in the form of salesbased or usagebased royalties on licences of intellectual property (Example 4) Example 1—Collectability of the consideration. IFRS 9 – Classification and measurement At a glance On July 24, 14 the IASB published the complete version of IFRS 9, Financial Instruments, which replaces most of the guidance in IAS 39 This includes amended guidance for the classification and measurement of financial assets by introducing a.

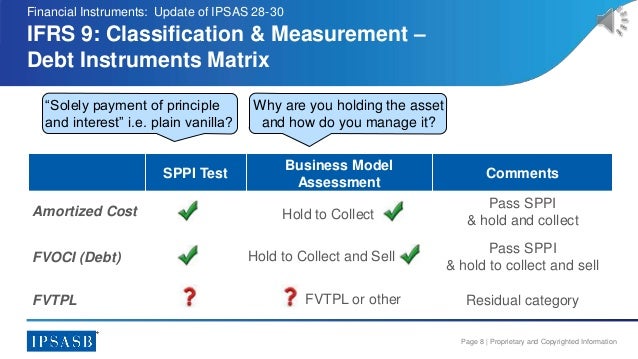

Of IFRS 9 or IAS 39 to hedges of interest rate risk affected by interest rate benchmark reform, and those who use their financial statements A summary of the proposals in this Exposure Draft The proposals in this Exposure Draft modify specific hedge accounting requirements so. IFRS 9 requires the classification of financial assets to be determined based on both the business model used for managing the financial assets and the contractual cash flow characteristics of the financial asset (also known as SPPI) There was no change from IAS 39 to IFRS 9 for the classification and measurement of financial liabilities. IFRS 9 – Classification and measurement At a glance On July 24, 14 the IASB published the complete version of IFRS 9, Financial Instruments, which replaces most of the guidance in IAS 39 This includes amended guidance for the classification and measurement of financial assets by introducing a.

The International Financial Reporting Standards Foundation is a notforprofit corporation incorporated in the State of Delaware, United States of America, with the Delaware Division of Companies (file no ), and is registered as an overseas company in England and Wales (reg no FC) Head office Columbus Building, 7 Westferry. Ifrs 9 1 AVC Learning Solutionswwwavclscominfo@avclscom91 0014 55 2 Financial InstrumentsIAS 32 / 39 / IFRS 9. With the help of Capterra, learn about IFRS 9 Impairment Solution, its features, pricing information, popular comparisons to other Banking Systems products and more Still not sure about IFRS 9 Impairment Solution?.

IFRS1 Australia, New Zealand and Israel have essentially adopted IFRS as their national standards2 Brazil started using IFRS in 10 Canada adopted IFRS, in full, on Jan 1, 11 Mexico will require adoption of IFRS for all listed entities starting in 12 Japan is working to achieve convergence of IFRS and began permitting certain qualifying. The IFRS Foundation provides free access (through Basic registration) to the PDF files of the current year's consolidated IFRS ® Standards (Part A of the Issued Standards—the Red Book), the Conceptual Framework for Financial Reporting and IFRS Practice Statements, as well as available translations of Standards This section also provides highlevel and nontechnical summaries for the. Listing of International Financial Reporting Standards International Financial Reporting Standards are developed by the International Accounting Standards Board Access to IFRS technical summaries and unaccompanied standards (the core standards, excluding content such as basis for conclusions) is available for free from the IASB website.

New ifrs 9 1 Accounting for financial instruments IFRS 9 2 2 »Classifying financial instruments »Recognising and derecognising financial assets »Impairment of financial assets Note other aspects of accounting for financial instruments have been covered in other sessions at this workshop Overview 3 Definitions 4. BOZ IFRS 9 Guidance Note & Deferment of Compliance with Corporate Governance Directives Dear esteemed member, The Bank of Zambia has issued circulars on implementation of IFRS 9 for regulatory purposes and Deferment of Compliance with Corporate Governance Directives To access these two (2) documents, you can follow the links below and download. IFRS 9 states that firms shall apply a definition of default consistent with the definition used for internal credit risk management purposes However, there is a rebuttable presumption that a default does not occur later than when the instrument is 90 days pastdue The firm may rebut the presumption if it has reasonable and supportable.

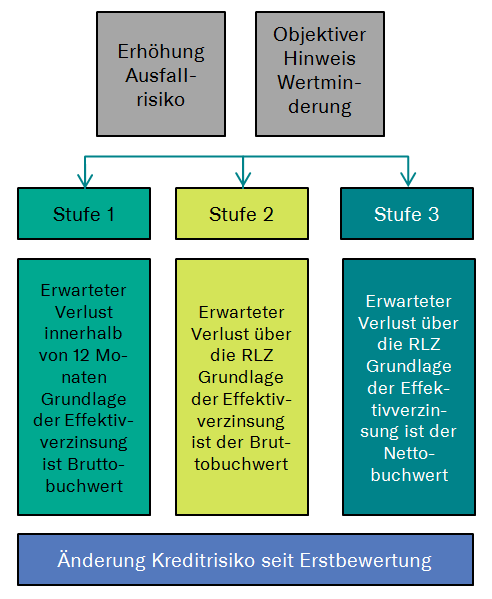

IFRS 9 IFRS 9 is the new international financial reporting standard for financial instruments, replacing IAS 39, and is applicable from 1 January 18 (with early application permitted) The principal updates of IFRS 9 relate to Classification and measurement classification of financial instruments is now driven by cash flow characteristics and the business model inRead More. The ESMA statement is broadly aligned with the guidance provided by the PRA and emphasises that assessing whether credit risk has increased significantly is a holistic assessment of a number of quantitative and qualitative factors and should capture changes in lifetime risk of default ie over the entire expected lifetime of the instrument It also provides guidance on accounting for. IFRS 9 requires the institution to consider, where pertinent, the evolution of credit quality to maturity, which, from a risk management perspective, is a more transparent approach This approach should, in addition to satisfying the regulators, lead to better credit approval decisions, which also will improve over time as the supporting data.

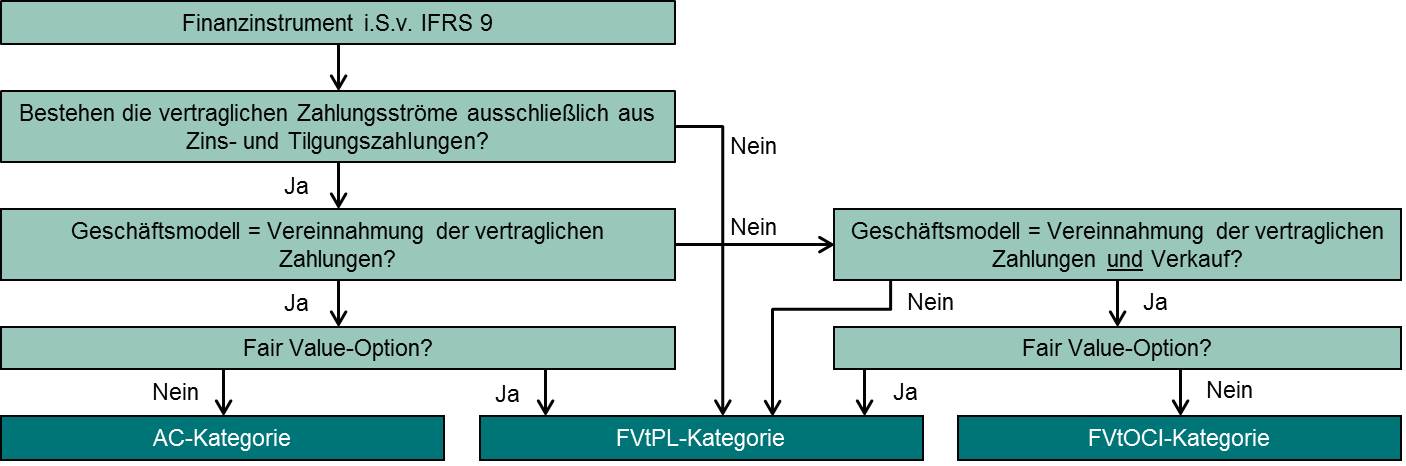

IFRS 9 Finanzinstrumente aus der Sicht von Industrieunternehmen 9 Grundsätzlich kann davon ausgegangen werden, dass PlainVanillaObligationen den SPPITest bestehen Zinszahlungen sind fixiert über die gesamte Laufzeit oder werden quartalsweise, halbjährlich oder jährlich aufgrund des ent. (a) the interaction of paragraph 9 of IFRS 15 with paragraphs 47 and 52 of IFRS 15 on estimating variable consideration (Examples 2–3);. (c) financial instruments and other contractual rights or obligations within the scope of IFRS 9 Financial Instruments.

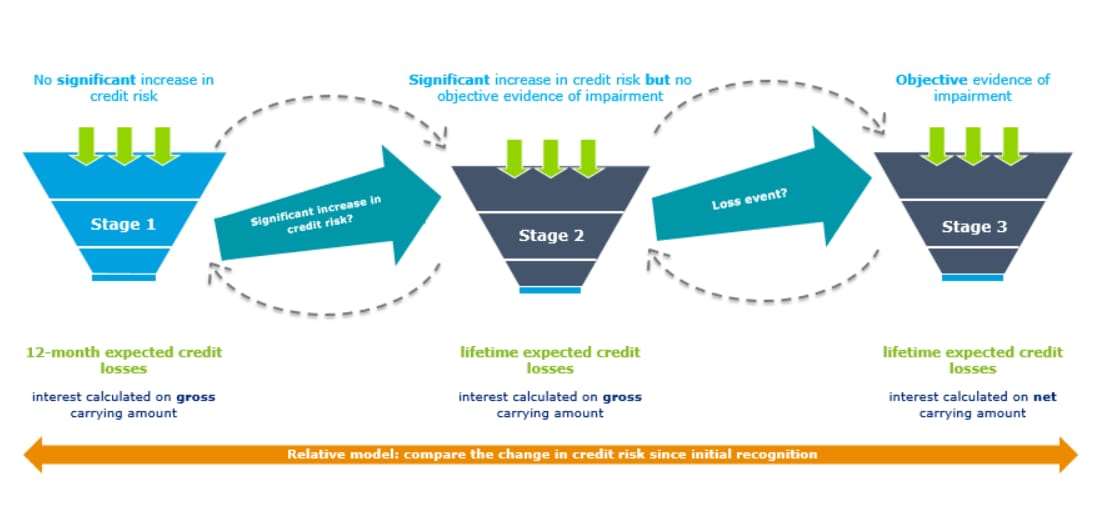

Scope 5 An entity shall apply this Standard to all contracts with customers, except the following (a) lease contracts within the scope of IAS 17 Leases;. The revised manual takes into account the new approach set out in IFRS 9 to impairments of bank assets and classifying financial instruments The assessment of provision levels on credit exposures follows the IFRS 9 staging model, which introduces the concept of “significant increase in credit risk since initial recognition” of a financial. These Guidelines have been developed in accordance with of the new Article 473a, paragraph Eight, included in the Proposal for a Regulation of the European Parliament and of the Council amending Regulation (EU) No 575/13 as regards the transitional period for mitigating the impact on own funds of the introduction of IFRS 9 and the large exposures treatment of certain public sector exposures.

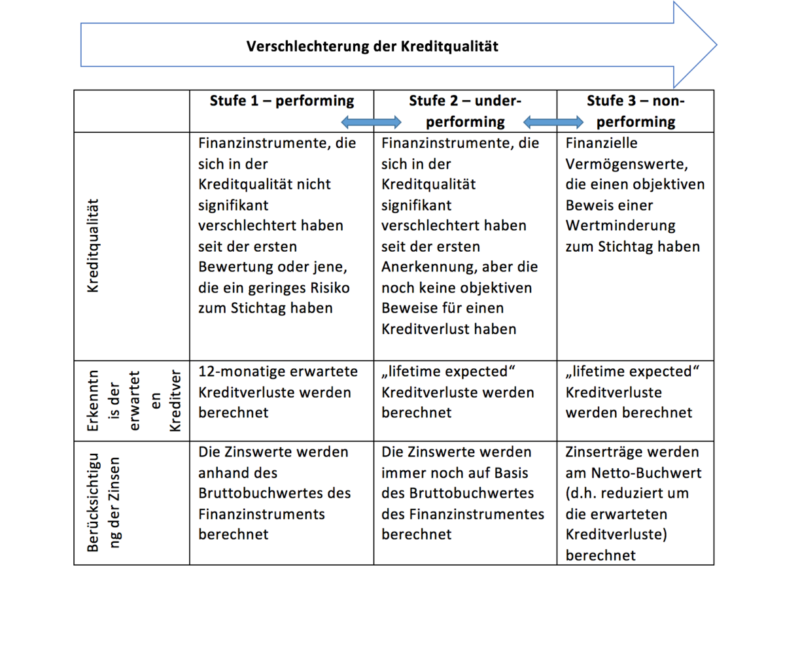

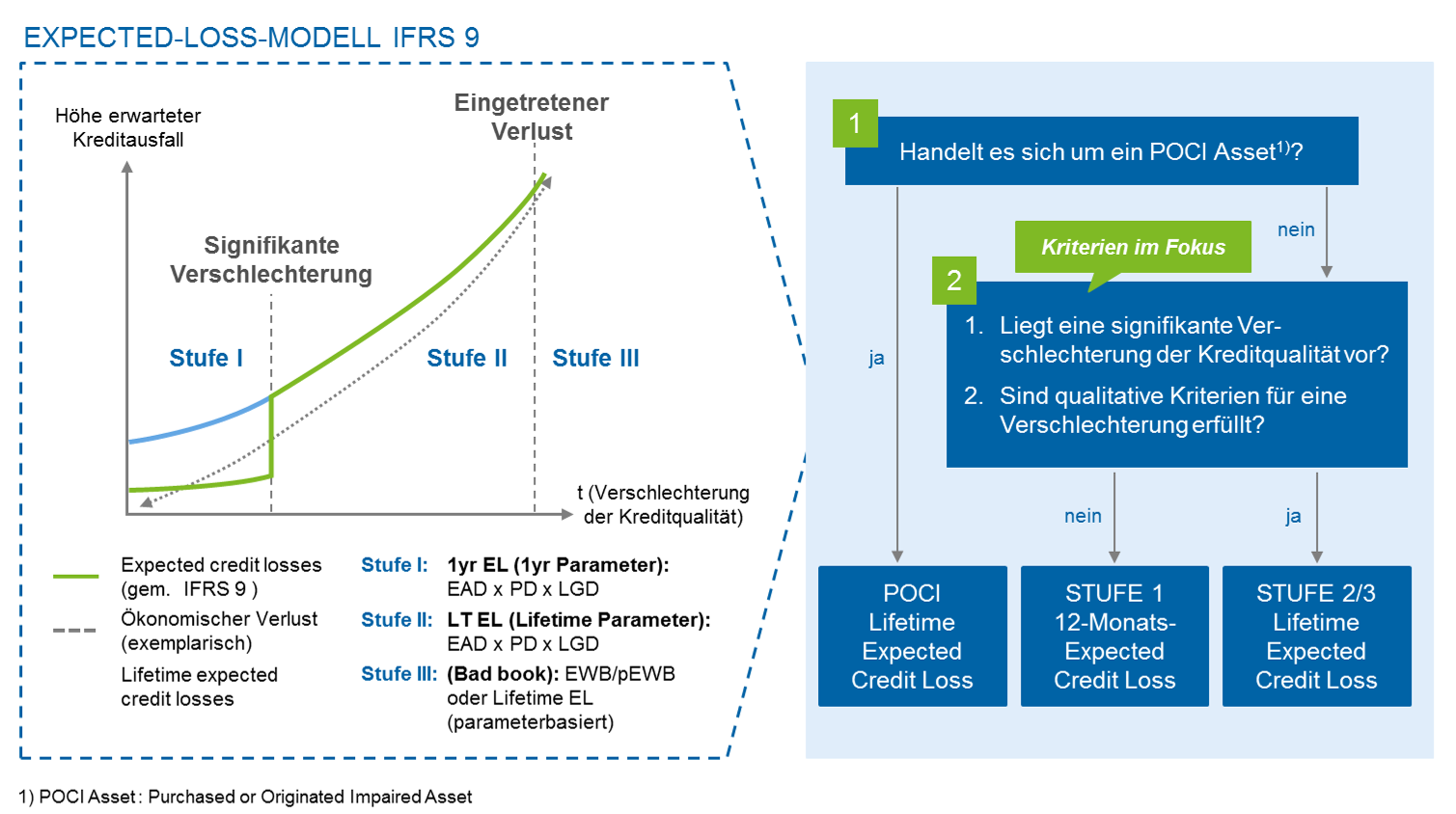

4 Im IFRS 9 werden der Stufe 2 die Finanzinstrumente zugeschlüsselt, welche sich seit Zugang wesentlich verschlechtert haben (Significant deterioration) 4 IFRS 9 – Financial Instruments 5 Strategie Geschäftsmodell Entsprechend der Regularien nach IFRS 9. (b) insurance contracts within the scope of IFRS 4 Insurance Contracts;. IFRS 9 and CECL Credit Risk Modelling and Validation A Prac £4761 starrating (13) International Financial Reporting Standards (IFRS) Deutsch £2495 starrating.

Welcome to EYcom In addition to cookies that are strictly necessary to operate this website, we use the following types of cookies to improve your experience and our services Functional cookies to enhance your experience (eg remember settings), Performance cookies to measure the website's performance and improve your experience, Advertising/Targeting cookies, which are set by third. 17, IFRS 9 and IFRS 7 may be met but are not intended to provide any view on the type of approach that should be applied The publication is current as of February 19 and is based on IFRS 17 as issued by the International Accounting Standards Board in May 17 It is prepared for illustrative. IFRS 9 – Classification and measurement At a glance On July 24, 14 the IASB published the complete version of IFRS 9, Financial Instruments, which replaces most of the guidance in IAS 39 This includes amended guidance for the classification and measurement of financial assets by introducing a.

IFRS 9 Financial Instruments has brought fundamental changes to financial instruments accounting in recent years Our materials will help you understand the requirements of this standard as they relate to your company, as well as offering insights and guidance on the application of IFRS ® Standards. IFRS 9 introduces new requirements on how an entity should classify, measure and reflect impairments to financial instruments The Transition Report summarises the impact of the implementation of IFRS 9 on shareholders’ equity, Risk Weighted Assets (RWA), regulatory capital, and key ratios for Deutsche Bank Group. IFRS 9 and the complete ‘IFRS 9 for banks – Illustrative disclosures’ can be found at informpwccom We hope accountants, modellers and others involved in IFRS 9 implementation projects find this publication both practical and useful If you have any questions on the publication, or on other matters related to IFRS 9,.

The new standard, IFRS 9, improves the decisionusefulness of the financial statements by better aligning hedge accounting with the risk management activities of an entity IFRS 9 addresses many of the issues in IAS 39 that have frustrated corporate treasurers In doing so, it makes some fundamental changes to the current.

Prepare Ifrs 9 Ecl Model Using Both General And Simplified Approach By Basit

Kpmg Nigeria Classification And Measurement Of Financial Assets In The Scope Of Ifrs 9 Africaifrsacademy T Co Huhoia3yok

Konzernanhang Puma Annual Report 17 Forever Faster Puma

Ifrs 9 Deutsch のギャラリー

Ifrs 9 Financial Instruments

International Financial Reporting Standards Ifrs 9 Linkedin

Pwc Cambodia In Brief Ifrs 9 Impairment Facebook

Ifrs 9 Impairment Konkretisierung Der Umsetzungsanforderungen Bankinghub

Read Ifrs 9 And Cecl Credit Risk Modelling And Validation Online By Tiziano Bellini Books

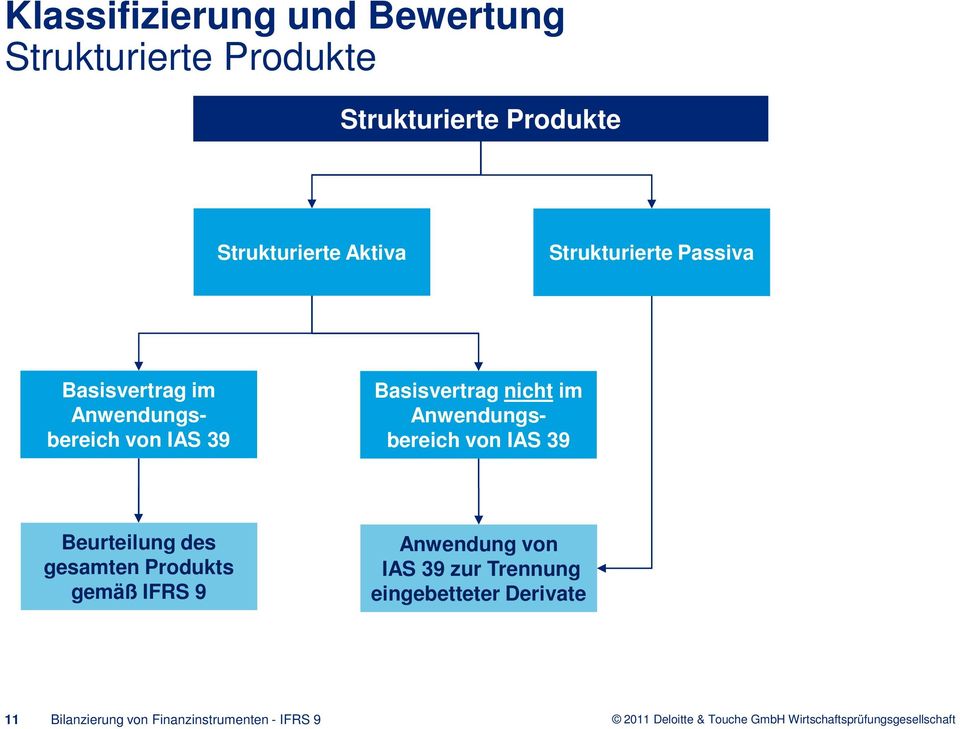

Ifrs 9 Ansatz Ausbuchung Und Modifizierung

Iasb And Regulators Highlight Ifrs 9 Ecl Requirements In Coronavirus Pandemic Pagetitlesuffix

How To Make Sense Of Transition To Ifrs 9 Expected Credit Loss Model Ey Global

Die Bewertungskategorien Des Ifrs 9 Amazon Co Uk Sibold Pit Books

The Impact Of Ifrs 9 On Banking Sector Regulatory Capital Deloitte Switzerland Financial Services Insight

Ifrs 9 Als Nachfolgestandard Des Ias 39 Grin

New Ifrs 9

Eur Lex 316r67 Lt Eur Lex

Ifrs 9 Financial Instruments High Level Summary Deloitte Cis Audit

Q Tbn And9gcteo6ohvzg7puo7zskf631gszrcgwvgx0gys9j0wplylw3ol2ly Usqp Cau

International Financial Reporting Standards Ifrs 9 Linkedin

Hedge Accounting Nach Ifrs 9 German Edition Lotz Marcus Amazon Com Books

Ifrs 9 Eroffnet Chancen Fur Die Portfoliostruktur

Ifrs 9 Impairment Practical Implications Protiviti Saudi Arabia

Ifrs 9 Financial Instruments

Ifrs 9 General Hedge Accounting Deloitte Deutschland

Ifrs 9 And Ecl Cva Services Gmbh

Baker Tilly Hk From The Archives Ifrs 9 Specifies How An Entity Should Classify And Measure Financial Assets Financial Liabilities And Some Contracts To Buy Or Sell Non Financial Items T Co Fc7qniup0g

Ifrs 9

Ifrs 9 Risk Audit

Ifrs 9 Im Ubergang Von Theorie Zu Praxis Rodl Partner

Ifrs

Financial Instruments Education Session Part A

Ifrs 9 Impairment Ein Blick Uber Den Tellerrand Der Lifetime Loss Modellierung Bankinghub

Validation Of Ifrs 9 Models

Bol Com Kritische Analyse Von Ansatz Und Bewertung Der Finanzinstrumente Im Rahmen Des Ifrs 9

Hedge Accounting Nach Ifrs 9 German Edition Lotz Marcus Amazon Com Books

Hedge Accounting Kritischer Vergleich Des Ias 39 Und Ifrs 9 Grin

Ifrs 9 And Ecl Cva Services Gmbh

Neue Internationale Regelungen Zur Klassifizierung Und Finanzinstrumenten Ifrs 9 Saarbrucken 19 Mai Martin Kopatschek Partner Pdf Free Download

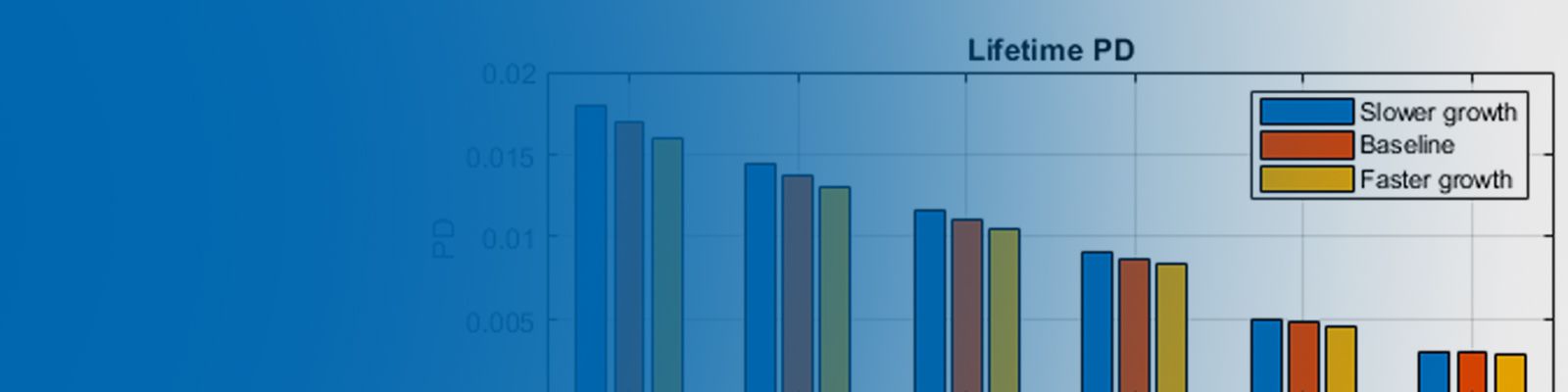

Cecl And Ifrs 9 Modeling In Matlab Measuring Lifetime Expected Credit Losses Matlab Simulink

Challenges Of Ifrs 9 Impairment Requirement To Prepare Early For The New Impairment Approach Bankinghub

Moody S Offers Riskintegrity Ifrs 17 Software For Insurers Preparing For Reporting Standards The Digital Insurer

Ifrs 9 Financial Instruments Overview

Ifrs 9 Impairment Konkretisierung Der Umsetzungsanforderungen Bankinghub

Zbam9t27vrui5m

Bilanzierung Nach Ifrs 9 Im Uberblick Deloitte Deutschland

Ifrs 9 Impairment Konkretisierung Der Umsetzungsanforderungen Bankinghub

Ifrs Hot Topic New Standards

Ifrs

Q Tbn And9gcr79qqrjgrb3ar3fzlqfgx9v I2hlqooektpmstevuwyooia98j Usqp Cau

Ifrs 9 For Corporates Is The Grass Greener On The Other Side

Ifrs 9 Financial Instruments Overview

How To Make Sense Of Transition To Ifrs 9 Expected Credit Loss Model Ey Global

Neue Internationale Regelungen Zur Klassifizierung Und Finanzinstrumenten Ifrs 9 Saarbrucken 19 Mai Martin Kopatschek Partner Pdf Free Download

Q Tbn And9gcrkdrbqx5zjyfhms0okf49mlrgq151q5mk5ckkehhg5myl7xnyv Usqp Cau

Deloitte Webinar The Impact Of Covid 19 On Assessing The Impairment Of Financial Instruments In Accordance With Ifrs 9

Ifrs 9 Overview For All Accountants

Www Bundesbank De Resource Blob 71c8cf60bc9784d052a5d5afd810f0d1 Ml 19 01 Ifrs9 Data Pdf

Mns Ifrs 9 11 Translation English Deutsch Francais Italiano By Gretk417 Issuu

Loan Valuations In The Age Of Expected Loss Provisioning Vox Cepr Policy Portal

Modelling For Provisioning Of Bad Debt Under Ifrs 9

Ifrs 9 For Corporates Is The Grass Greener On The Other Side

Ifrs 9 Financial Instruments

Pkf Polska

Ifrs 9 Eine Zusammenfassung Verovis

Ifrs 9 Finanzinstrumente Institut Fur Rechnungslegung

File Ifrs9 Classification Png Wikimedia Commons

Ifrs 9 Finanzinstrumente Youtube

Ifrs 9 Solution For Sap Trm Fam Compiricus

Financial Assets Under Ifrs 9 The Basis For Classification Has Changed o Australia

Ifrs 9 For Corporates Is The Grass Greener On The Other Side

Financial Assets Under Ifrs 9 The Basis For Classification Has Changed o Australia

Credit Impairment Under Ifrs 9 For Banks

Ifrs 9 Finanzinstrumente Onlinekurs Videoausschnitt Ifu Online Campus De Youtube

Ifrs 9 Wikipedia

Ifrs 9 Financial Instruments High Level Summary Deloitte Cis Audit

Sap Bank Analyzer Afi

Challenges Of Ifrs 9 Impairment Requirement To Prepare Early For The New Impairment Approach Bankinghub

Ifrs 9 Ind As 109 Impairment Of Financial Asset

Ifrs 9 Overview For All Accountants

Ifrs 9 Ready For Impact Deloitte Middle East Me Pov Issue 24

Bilanzierung Aktuelles Zur Internationalen Rechnungslegung Ifrs 9 Icon Wirtschaftstreuhand Gmbh

Fas Ag Ifrs 9 Finanzinstrumente

Ifrs 9 Impairment Practical Implications Protiviti Saudi Arabia

Ifrs 9

Ifrs 9 Financial Instruments Reporting Solutions November 17

After The First Year Of Ifrs 9 Deloitte Uk

How The Decl Recommendations On Ifrs 9 Could Affect Credit Risk Disclosures Ey Global

Ifrs 9 Ind As 109 Impairment Of Financial Asset

Ifrs Foundation Ifrsfoundation Twitter

Implementation Of The Expected Credit Loss Model Kpmg Germany

Ifrs 9 For Corporates Is The Grass Greener On The Other Side

Ifrs 9 Summary Requirements Changes Deloitte Cfr

Challenges Of Ifrs 9 Impairment Requirement To Prepare Early For The New Impairment Approach Bankinghub

Ifrs 9

Heads Up Iasb Completes Its Project On Accounting For Financial Instruments Under Ifrs 9

Ifrs Foundation Ifrsfoundation Twitter

Download E Book How To Model And Validate Expected Credit Losses For Ifrs 9 And Cecl

Ifrs 9 Finale Fassung Zur Bilanzierung Von Finanzinstrumenten Rodl Partner

Zbam9t27vrui5m

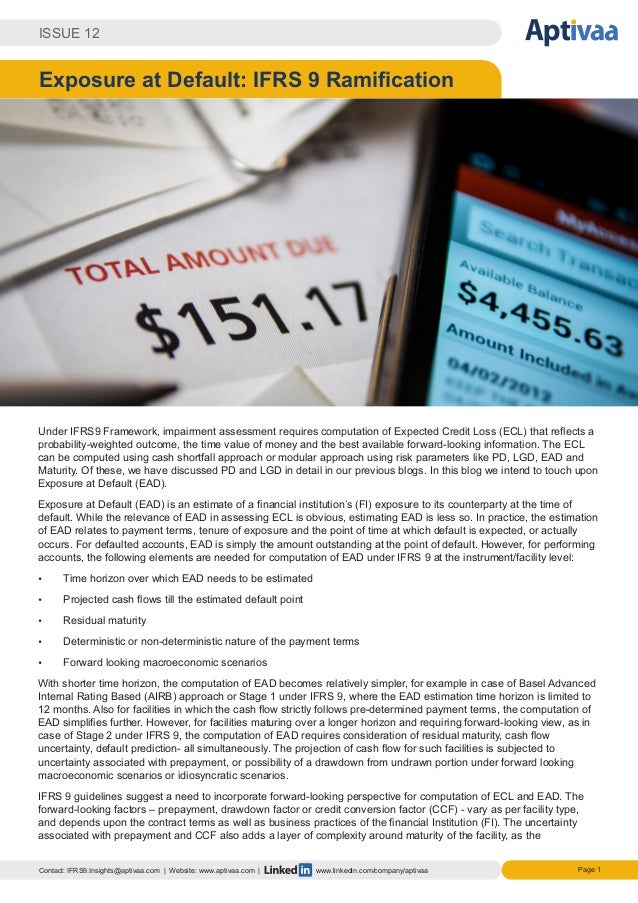

Blog 16 12 Ead Ifrs 9 Ramifications

Hedge Accounting Nach Ifrs 9 German Edition Lotz Marcus Amazon Com Books

Disclose Update Ifrs 9 Betrifft Alle Ifrs Anwender

Ifrs 9 Impairment Ein Blick Uber Den Tellerrand Der Lifetime Loss Modellierung Bankinghub